Large companies that are leading the market are financially solid. Investors that have been shaken off of stocks over the past 2 severe corrections, 2000 and 2009, are growing restless. In fact investors are eager to buy any dips the market gives them. Cash is building, the market is climbing, and few analysts have joined the bandwagon that this move is sustainable. Prudent rhetoric continues to call for caution, yet those warnings also continue to be wrong. Sure, they will be right eventually.

Bear Markets occur when the broad indexes drop 20%. This rule is not a rule however, it is just a guideline. Last year, in late February, the S&P 500 corrected 13.3%. This followed a similar correction in 2015. While each of these overall did not meet the ‘rule’ of a bear market, each of those corrections created bearish sentiment and gave investors reason to stay away. The correction stalled apparently when sellers were not willing to part with more shares, and the market began to recover. This is a very common trait to the end of bear markets, but these corrections in back to back years might just have been the bear market many have been calling for, albeit not by the ‘rule’.

Why have so many experts been wrong about the direction of stock prices? There are many reasons, but as most of us know, this bodes well for more gains as the market usually goes in the direction most people are not expecting. Volatility of share prices are historically low. While I must admit this concerns me too, it sort of makes sense. Retail investors that are chasing their usual ‘hot stocks’ have been rewarded. Value investors have been in a prolonged drought….while the indexes make new highs. Their frustration compounds as their performance lags.

The S&P index funds hold 20% of the money in only 10 stocks of the 500 in the index. It is hard to beat that weighted index as long as those 10 stocks continue to outperform. While sidelined cash continues to be converted to into investments, from real estate to stocks and even bonds, this is not euphoric as it was in the late 90’s, even though some of the valuations are compared with that time frame.

Where else do you invest? Real Estate is seeing lots of activity, yet housing starts are still historically low. While apartments and condo projects are going up in most all major cities, demand appears robust enough to potentially avert severe overbuilding. Bond yields are historically low, and attempts to push interest rates higher have failed so far. Precious metals typically like low interest rates, but they have been slow to move, even with North Korea’s nuclear chatter. Private market valuations are high, as that game is played by the professionals and there are plenty of investors at valuations usually reserved for an IPO. Speaking of those, 2016 saw funds raised in IPOs drop 66% from the levels of 2015. That type of statistic is common during bear markets, not aging bull markets. This could be more evidence that we might have already had the correction so many fear, yet the rising tide has been slow to float all boats.

The general lack of enthusiasm as the market makes new highs is unusual if this is a bubble. Investors continue to try not to hold onto cash but can’t help themselves. There is a lack of performance by hedge funds and money managers picking individual stocks. Stock buybacks have slowed down. Merger activity is low, and has been for a couple of years. Has a moat been built around the market already? You might say CEOs are worried, judging them by what they are not doing and not by what they are saying. Acquiring a company in this environment at a high valuation would sure look foolish if the correction is just around the corner. This is creating a standoff of sorts. Earnings reports have met or exceeded expectations generally, while interest rates are very low and almost no one is calling for a raging bull market. It’s a Perfect Calm. This can and will change, but for now, steady as she goes!

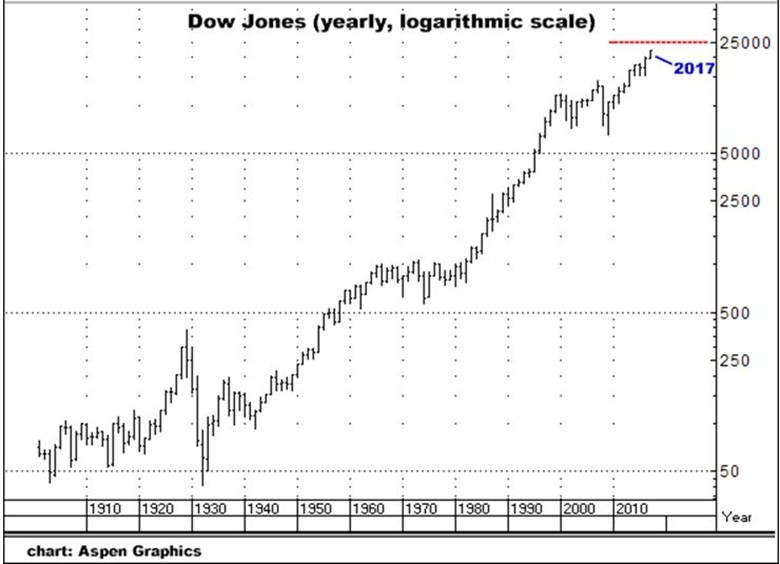

Each line on this chart represents one year. Notice how narrow this year has been compared to previous years. Of course the year is not over.