Latest Comments by Bobbo Jetmundsen

The sudden volatility of the markets over the last week or so shows that investors remain nervous and willing to hold even more cash than they have already stockpiled. China came back into the spotlight, and focus is trying to shift away from Fed. Chairman Yellen and Greece to eventually somewhere else. Caution has been the attitude, for the most, part ever since the bust of the Dot Com bubble and subsequent bottom in late 2002. The market correction ended then at around 7500 on the DJIA, now 13 years ago. Interestingly, that nervous attitude may not have cost them much….yet. Daytime business TV has continued to have a profound impact on viewers, giving them, ‘the herd’, the same story to fret over. You can’t easily become street smart by watching business TV. Don’t get me wrong, I watch a little myself, and there are some wonderful thoughts given by very smart and savvy investors worth hearing. So I can’t fault you for tuning in, and actually do encourage it, but be careful to know who is saying what and for what reason. A trader thinking the market is about to drop 5% is different from someone who is a long-term investor thinking ‘so what if it does’.

This is the year before a Presidential election where there is not an incumbent on the ballot, and that occurred in 1987 and 2007, both years where the market ran into significant trouble. It seems that this is an ingredient of uncertainty that has a history of creating a sell off. Today we wonder if Hillary will survive and when Trump will falter. We must expect that there will be more volatility, and you should too. Even if the economy slows, the momentum has been impressive, and a potential recession seems unlikely to be severe. Rhetoric from some of the candidates continues to suggest that capital gains rates will go up. Investors may be anticipating that already, locking in current rates by selling shares.

Technology not only creates new opportunities, it also drives existing costs/prices down. Look how much value you get today for a new TV or car. So while I too see the lackluster growth in revenues on the S&P, I know some of that is because of technology, which is a good reason. Commodity prices are now (ok, eventually) approaching a capitulation phase; meaning the drop in prices for oil, aluminum, copper, gold and so on are probably nearing a bottom. The forces pushing down the price of oil on the exchanges and what we pay at the pump have been creating immediate stimulus for our most needy lower and middle class drivers, small businesses and certainly helps the airlines and other large consumers of energy. At the same time, it causes major headaches for oil related industries and the oil producing countries including the USA which now produces 9.5 million barrels of oil a day. Russia and ISIS both use oil and gas for major sources of revenue, and that revenue is falling fast. I have no idea if the US Government actually manipulates prices of oil as some think Mr. Putin implied. If the threat of war is declining, then the purging of our military commanders that continues under this administration may be justified. (Google it). However, I am not so sure if this is good or bad, or what it means for a country with so many military elite out of work and likely not happy.

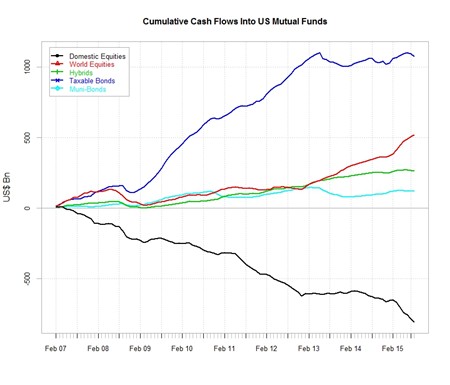

Many people look at the prices of stocks and think they are overvalued. But every time the market tries to fall, buyers show up, likely because they have cash and are under invested. Overall cash reserves still appear to be quite high, but we have noticed that stock mutual funds cash balances are declining as money has been flowing out.

(Chart: Pierre Org - www.argonautae.com)

I do not like a trend I see of management sugar coating their problems, and spending company cash to buy back their shares. Some are using shareholder cash to keep analysts and others happy and telegraph that they really believe in themselves. A company should be only able to buy back shares once the management team is buying shares with their own money, and in some relationship that is relevant. At the very least, companies should measurably demonstrate their buyback is significantly beneficial to shareholders and accretive.

I have not ever experienced so many companies exceeding analysts’ estimates and then having their stock significantly sold off in the market. That’s quite unusual. I don’t know exactly why, but I suspect that investors are still interested in raising cash and had planned to use any good news to help them do that. You might have thought that the market was attempting to correct itself simply by not going up. Well, so much for that.

Energy stocks were being held as a staple in investors’ accounts (including ours) and are now being pushed out of portfolios at a rapid pace. I suspect when the energy sector has a very low weight to the S&P historically, there will be a bottom. Painfully we wait!

Stay the course. Hope you had a great summer!

-Bobbo Jetmundsen

Disclaimer: Worthscape, LLC does not guarantee the accuracy of completeness of this report, not does Worthscape, LLC assume any liability for any loss that my result from reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice and are for general information only. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. Reference to specific securities, issuers and data for illustrative purposes only.

Copyright © 2015 by Worthscape, LLC. All rights reserved. The information contained in this report may not be published, broadcast, or rewritten without prior consent from Worthscape, LLC